California First Time Homebuyers 2024 Guide

Understanding the California Real Estate Market

The California real estate market is shaped by a variety of economic factors, housing demand, supply trends, and regional market variations. Buyers, particularly first-timers, benefit from grasping these dynamics to make informed decisions.

Economic Factors Influencing Home Prices

Economic trends play a significant role in shaping home prices in California. Factors such as employment rates, income levels, and interest rates directly impact affordability and the overall health of the real estate market. For instance, a strong job market in technology sectors has historically driven up prices in the Bay Area.

Housing Demand and Supply Trends

The balance between demand and supply is a critical aspect of understanding the California housing market. High demand for homes, coupled with low inventory, tends to drive up property prices. This phenomenon is particularly evident in urban centers and popular neighborhoods where competition for housing can be fierce.

Regional Market Variations

California’s real estate market varies significantly by region. Coastal cities, such as San Diego, often have higher property values due to desirability and limited availability. Meanwhile, inland regions may offer more affordability but can be affected by different economic factors, such as agricultural or manufacturing sectors. Understanding these regional nuances is vital for prospective buyers.

Pre-Purchase Preparation

When embarking on the journey to homeownership, potential buyers must first ensure financial stability and awareness. The preparation stage includes assessing financial readiness, understanding credit score impacts, setting a budget, and saving for various associated costs.

Assessing Your Financial Readiness

A thorough assessment of one’s financial situation is the cornerstone of preparing to purchase a home. Prospective buyers should review their income, debt, expenses, and savings to determine if they are financially stable and ready to take on the responsibilities of homeownership.

Credit Score Importance and Improvement

A healthy credit score can significantly influence the terms of the mortgage loan, including the interest rate. Consumers need to check their credit score early and look for ways to improve it, such as paying down debts and avoiding new credit lines.

Setting a Realistic Budget

Homebuyers should establish a realistic budget that factors in their monthly income, existing debts, and the additional costs of owning a home, like property taxes and maintenance. A common recommendation is that housing should not exceed 30% of a buyer’s gross monthly income.

Saving for Down Payment and Closing Costs

Saving for a down payment is a crucial part of the home-buying process. Buyers typically need 20% of the home’s purchase price to avoid private mortgage insurance (PMI). Additionally, they should prepare for closing costs, which can range from 2% to 5% of the loan amount.

First-Time Homebuyer Programs in California

California offers various programs designed to help first-time homebuyers secure financing and achieve homeownership with more favorable terms than conventional loans.

State-Sponsored Loan Programs

California’s state-sponsored loan programs provide first-time homebuyers with several loan options. The CalHFA FHA loan is popular due to its fixed interest rate for a 30-year mortgage, backed by the Federal Housing Administration. Moreover, the CalHFA Conventional Loan Program offers similar benefits through conventional financing channels.

Down Payment Assistance

For those struggling with the initial costs of purchasing a home, California provides down payment assistance programs. The “MyHome Assistance Program” can be combined with other loan programs to offer additional support for the down payment and closing costs, making homeownership more accessible.

Tax Credits and Exemptions

First-time homebuyers in California may also benefit from various tax credits and exemptions, which can yield significant savings over time. The Mortgage Credit Certificate (MCC) program allows homebuyers to claim a percentage of their mortgage interest as a tax credit during the life of the loan, enhancing the affordability of buying a home.

Finding the Right Home

When embarking on the journey of purchasing their first home, buyers should focus on location, property type, and understand the fundamentals of home inspection and appraisal.

Choosing the Appropriate Location

The old adage “location, location, location” holds true in real estate. Prospective homeowners should consider factors like:

Proximity to Work: Commute times can impact daily life significantly.

School Districts: Quality of education is crucial for families.

Safety: Low crime rates are a top priority for most buyers.

Amenities: Access to shopping, parks, and other conveniences matters.

Resale Value Potential: Some areas appreciate more than others.

Helpful information for home buyers and borrowers includes insights into how each of these factors may affect their decision.

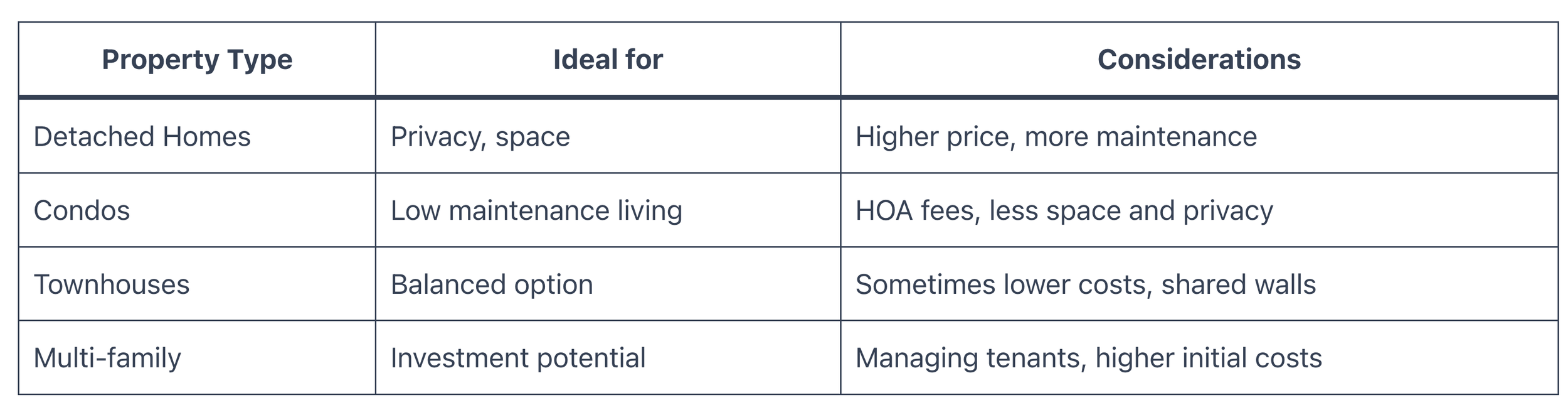

Evaluating Property Types

Different types of properties suit different needs and lifestyles. Buyers should assess:

They might also consider various government loan programs that can be more suited to certain property types and buyer situations.

Home Inspection and Appraisal Basics

Before sealing the deal, understanding inspection and appraisal processes is essential to ensure a smart investment. Buyers should:

Hire a Qualified Inspector: To identify potential issues with the property.

Understand Appraisal Value vs. Selling Price: An appraisal ensures they are not overpaying.

Plan for Possible Repairs: The inspection may reveal issues that can affect budgeting.

The California first-time home buyer programs and grants provide resources that can help first-time buyers navigate the complexities of inspections and appraisals.

The Mortgage Process Explained

Navigating the mortgage process is a critical step for California first-time home buyers. It involves understanding the pre-approval process, the variety of loan options and terms available, and how interest rates affect mortgages.

Mortgage Pre-Approval

Mortgage pre-approval is a lender’s preliminary assessment of a buyer’s financial situation, determining how much they can potentially borrow. Pre-approval involves submitting financial documents, such as tax returns, pay stubs, and bank statements, for review. The California Department of Real Estate advises that a strong credit score is often required, especially for programs like CalFHA, which stipulate a credit score typically between 660-680.

Understanding Loan Options and Terms

First-time buyers must familiarize themselves with various loan options, including conventional loans, FHA loans, and other programs tailored to first-time buyers. For instance, a common choice for those with lower credit scores is an FHA loan, which allows down payments as low as 3.5% for those with credit scores of 580 or higher. Each loan type offers different terms, like the length of the loan and whether it’s fixed-rate or adjustable.

Interest Rates and Their Impact

Interest rates directly influence the monthly payments and the overall cost of a mortgage. They vary based on market conditions, the borrower’s creditworthiness, and the specific loan product chosen. Higher interest rates result in higher monthly payments, whereas lower rates can offer significant long-term savings. Thus, tracking rate trends can be a key strategy for buyers as advised by resources like the California Housing Finance Agency.

Making an Offer and Negotiating

When approaching the task of making an offer on a property, first-time home buyers should understand the importance of a well-crafted bid, awareness of necessary disclosures and contractual contingencies, as well as effective negotiation techniques.

Crafting a Competitive Offer

A buyer’s initial offer is critical in catching a seller’s attention. This should be based on a thorough analysis of the local market to ensure it’s competitive yet not overpriced. Assistance from a real estate agent familiar with California’s intricacies can be valuable in this assessment. Offers should be commensurate with similar property sales in the neighborhood and align with the buyer’s predetermined budget.

Contingencies and Disclosures

An offer should always incorporate relevant contingencies and the buyer must understand any associated disclosures. Contingencies are specific conditions that must be met for the transaction to proceed, such as a satisfactory home inspection or final mortgage approval. Comprehensive disclosures may include material facts about the property’s condition, and California’s real estate laws are strict about ensuring these are communicated effectively. The DRE assists in regulating the disclosure requirements.

Negotiation Strategies for First-Time Buyers

Negotiation, a delicate dance of give-and-take, requires first-time buyers to be prepared yet adaptable. One should approach negotiations with clear objectives but also a readiness to compromise if necessary. Utilizing a skilled negotiator with experience in California’s housing market can be a game-changer, providing the expertise to secure a fair deal without overstepping budget constraints.

The Closing Process

The closing process in California is decisive for first-time homebuyers, involving a neutral third party that oversees the final transfer of funds and the property deed.

Understanding Escrow

Escrow refers to a legal concept where a neutral third party holds the assets during the transaction between the buyer and seller. In California’s housing market, escrow begins when the seller accepts the offer, and both parties sign a purchase agreement. The buyer then deposits their earnest money into an escrow account, which the escrow company holds until the transaction’s conditions, usually set by the lender or the buyer, are met. Notably, understanding the escrow closing process is essential for homebuyers to ensure they fulfill all the requirements before the big day.

Final Walkthrough and Closing Day Procedures

Final Walkthrough of the property typically occurs 24 hours before the closing date, allowing the buyer to inspect the property and verify that all agreed-upon repairs are completed. It’s crucial to use this final walkthrough to ensure no new issues have arisen.

On Closing Day, buyers will need to sign numerous legal documents, which include the deed, loan documents, and other related papers. A representative, usually from the escrow company or a signing agent, will guide homebuyers through each document. After signing, buyers will pay closing costs, often ranging between 3% and 7% of the home’s purchase price. These specifics are vital for potential homeowners to plan for accordingly. Familiarizing oneself with the required steps for closing day procedures prepares buyers for a smooth transaction, culminating in the keys to their new home.

Post-Purchase Considerations

After securing a new home, homeowners in California must be attentive to ongoing responsibilities to protect their investment. These include obtaining proper insurance, staying current with property taxes, and maintaining the condition and value of the home.

Homeowners Insurance

Homeowners insurance is a crucial safeguard for your property and assets. In California, it not only protects against natural disasters—which can include fires, earthquakes, and floods—but also against theft and liability. Careful evaluation of coverage options helps California homeowners choose a policy that best fits their needs.

What to Insure: Structure of home, personal belongings, liability for injuries on property.

Key Providers: Compare different insurance companies to find the best rates and coverage.

Property Taxes

Property taxes in California are recalculated at the time of purchase and reassessed annually. These taxes fund important local services such as schools, law enforcement, and parks.

Calculations:

Assessment: Typically 1% of the home’s purchase price.

Increases: Limited to 2% per year under Proposition 13.

Maintenance and Home Improvement

Regular maintenance ensures the longevity of a home and can prevent costly repairs in the future. Home improvement projects can further enhance a property’s value.

Maintenance Tips:

Perform seasonal checks: Inspect roofing and gutters; service the HVAC system.

Address minor repairs promptly to avoid more significant issues.

Improvements Considerations:

Prioritize upgrades that increase value, such as kitchen renovations or energy-efficient windows.

Obtain necessary permits for larger projects to ensure compliance with local regulations.

Building Home Equity

Building home equity is a critical financial strategy for homeowners. It involves increasing the homeowner’s financial stake in their property, which can benefit them significantly over the long term.

Mortgage Repayment Strategies

Paying down the mortgage principal is one of the most effective ways to build equity in a home. Homeowners can employ various repayment strategies to accelerate this process:

Additional Payments: Making extra payments directly toward the principal can reduce overall interest and shorten the loan term.

Refinancing: Sometimes, refinancing to a lower interest rate can allow more of each payment to go toward the principal rather than interest.

Leveraging Home Equity Responsibly

Once a homeowner has built up equity, it can be leveraged to access funds for various purposes. However, it is important to do so responsibly:

Home Equity Loans: These allow homeowners to borrow against the equity they’ve accumulated in their homes but should be used judiciously for significant expenses like home improvements.

Home Equity Lines of Credit (HELOCs): HELOCs provide a flexible line of credit, but caution is advised as they often come with variable interest rates.

Frequently Asked Questions

Navigating the world of real estate as a first-time home buyer in California can be complex. These FAQs aim to clarify common queries related to assistance programs, down payments, mortgage options, credit requirements, and specific state-provided aids to help make homeownership more accessible.

What assistance programs are available for first-time home buyers in California?

California offers various assistance programs for first-time home buyers, including down payment assistance, affordable first mortgage loans, and other programs that can help ease the financial burden.

How much down payment is required for a first-time home buyer in California?

The down payment requirement for first-time home buyers in California can vary, but programs exist that allow as little as 0% down for qualified buyers.

Are there special mortgage options for low-income first-time home buyers in California?

Yes, low-income first-time home buyers in California may qualify for special mortgage options, such as the CalPLUS FHA program, which includes a zero-interest program for down payment assistance.

What are the credit score requirements for first-time home buyers in California?

Credit score requirements for first-time home buyers in California vary by lender and program, but a minimum score of 620 is typically needed for most conventional loans.

How does the CalHFA program assist first-time home buyers?

The CalHFA program assists first-time home buyers by offering various types of loans and grants that can be used for down payment and closing costs, in addition to providing educational resources.

What are the income limits for first-time home buyer programs in the Bay Area, California?

Income limits for first-time home buyer programs in the Bay Area vary, but CalHFA’s income limits can provide a guideline, as they are adjusted annually to reflect current median incomes and cost of living in specific areas.

This article originally appeared on ark7.com. See the original article HERE.